How much you can leverage a cost segregation study is largely dependent on what state your property is in. The reason for this is simple: not all states recognize the federal bonus depreciation rate.

In states like Texas and Utah, which do recognize federal bonus depreciation at the state level, you will be able to take the benefits of bonus depreciation on both your federal and state tax returns. However, in states like California, which do not recognize federal bonus depreciation at the state level, you will not be able to take bonus depreciation on your state tax return.

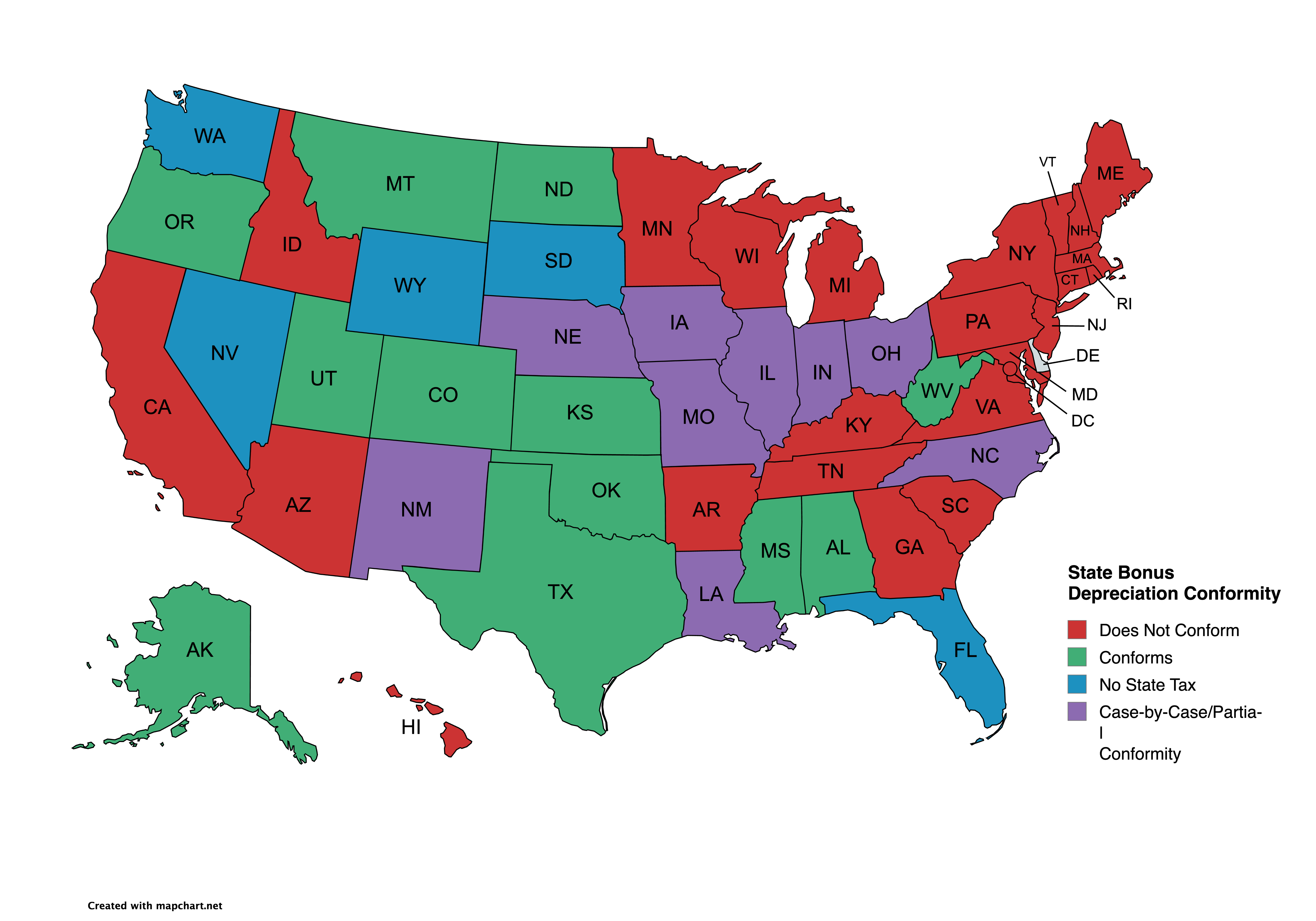

States That Do Not Conform

The following states do not conform to federal bonus depreciation:

- Arizona, Arkansas, California, Connecticut, D.C., Georgia, Hawaii, Idaho, Kentucky, Maine, Maryland, Massachusetts, Michigan, Minnesota, New Hampshire, New Jersey, New York, Pennsylvania, Rhode Island, South Carolina, Tennessee, Vermont, Virginia, Wisconsin

In states that do not conform to federal bonus depreciation, the federal return may allow an immediate bonus depreciation deduction, while the state return may require the taxpayer to add back or disallow that bonus amount and depreciate the assets over a separate state schedule. This does not eliminate the federal benefit, but it can reduce or delay the state-level benefit.

This does not keep taxpayers from finding meaningful benefit in getting a study done and front-loading a portion of depreciation to the early years. It just will not be as immediately impactful as taking bonus depreciation in a state that does conform would be.

States That Do Conform

- Alabama, Alaska, Colorado, Kansas, Mississippi, Montana, Nebraska, North Dakota, Oklahoma, Oregon, Texas, Utah, West Virginia

If your depreciable property is in one of these states, you can take full advantage of bonus depreciation on both your federal and state tax returns. Properties placed in service in 2025 and 2026 are eligible for 100% bonus depreciation, meaning all your 5- and 15-year property can be accelerated on both the federal and state level.

The remaining hurdle is making sure you have enough of the right kind of income to absorb the deduction. That typically means passive income from other investments, or Real Estate Professional status, which allows the accelerated depreciation to offset your W-2 income (or your spouse's).

States With No State Income Tax

- Florida, Nevada, South Dakota, Washington, Wyoming

Because these states have no income tax, bonus depreciation has no state-level impact. Your federal return still gets the full benefit, but there is nothing on the state side to conform or deviate from.

States That Conform on a Case-by-Case Basis

- Delaware, Illinois, Indiana, Iowa, Louisiana, Missouri, New Mexico, North Carolina, Ohio

These states follow federal bonus depreciation rules to varying degrees. If your property is in one of these states, you will want to verify the current rules with a local CPA or tax advisor, since the state-level treatment can differ meaningfully from what you receive on your federal return.

Final Takeaway

The reason investors love cost segregation, especially in recent years, is the immediate impact it can have in year one. On a $500,000 property, it is not uncommon for a cost segregation analyst to identify over $75,000 in short-term personal property. Depending on the state the property is in, that deduction can range from significant to extraordinary, particularly in states where 100% bonus depreciation applies at both the federal and state level.

Whether you are in a conforming state, a non-conforming state, or somewhere in between, understanding where your state lands on bonus depreciation is an essential part of projecting the true value of a cost segregation study. The rules are not uniform, and the difference between a conforming and non-conforming state can translate into tens of thousands of dollars on a single acquisition.

If you are unsure how your state treats bonus depreciation, or whether a cost segregation study makes sense for your specific situation, consult a qualified tax professional or reach out to us for a free consultation.